The U.S. Electrical Contracting industry represents a large, essential, and steadily growing segment of the broader construction and infrastructure services economy. Demand is supported by sustained commercial construction activity, public infrastructure investment, energy-efficiency upgrades, and accelerating adoption of electrification technologies including EV charging, solar installations, and smart-building systems.

While the industry remains highly fragmented and labor-constrained, well-established electrical contractors with strong project pipelines, diversified end markets, and experienced management teams continue to attract meaningful buyer interest from strategic consolidators, private equity-backed platform contractors, and infrastructure-focused investors.

For business owners, current market conditions present an attractive valuation environment. Structural demand tailwinds, government-supported infrastructure spending, and increasing technical complexity in electrical work are driving consolidation — favoring professionally managed operators with scale, backlog visibility, and skilled labor retention.

Electrical contracting is a foundational trade within the U.S. construction ecosystem, delivering wiring, power distribution, lighting, controls, and system integration across nearly every building and infrastructure project. As facilities become more electrified and automated, electrical contractors play an increasingly central role in construction delivery.

According to IBISWorld and Business Valuation Resources data:

The industry remains highly fragmented, with the vast majority of operators generating under $2 million in annual revenue. This fragmentation has fueled a multi-year consolidation cycle, as buyers seek scale efficiencies, expanded licensing footprints, and improved bidding and project management capacity.

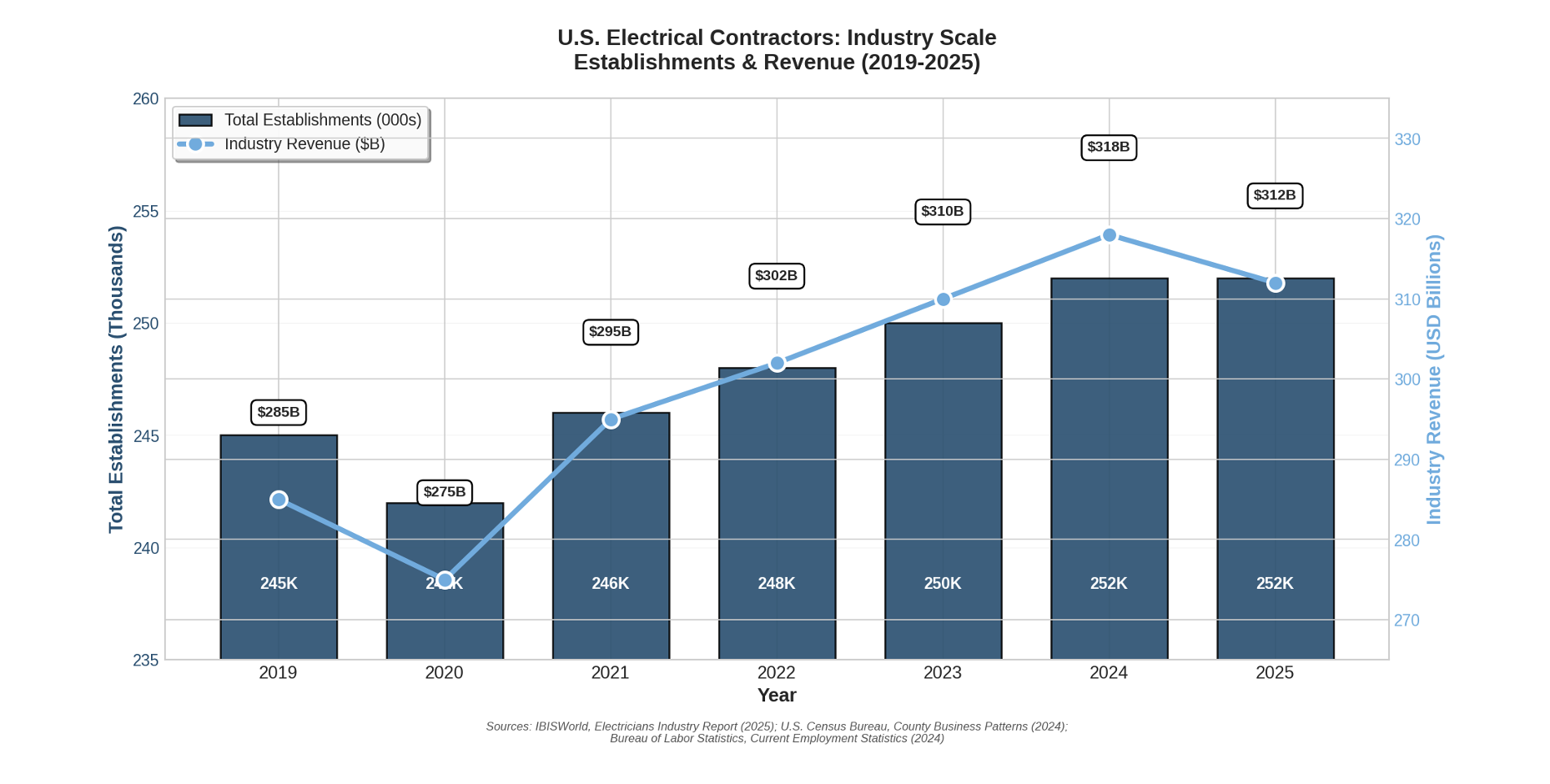

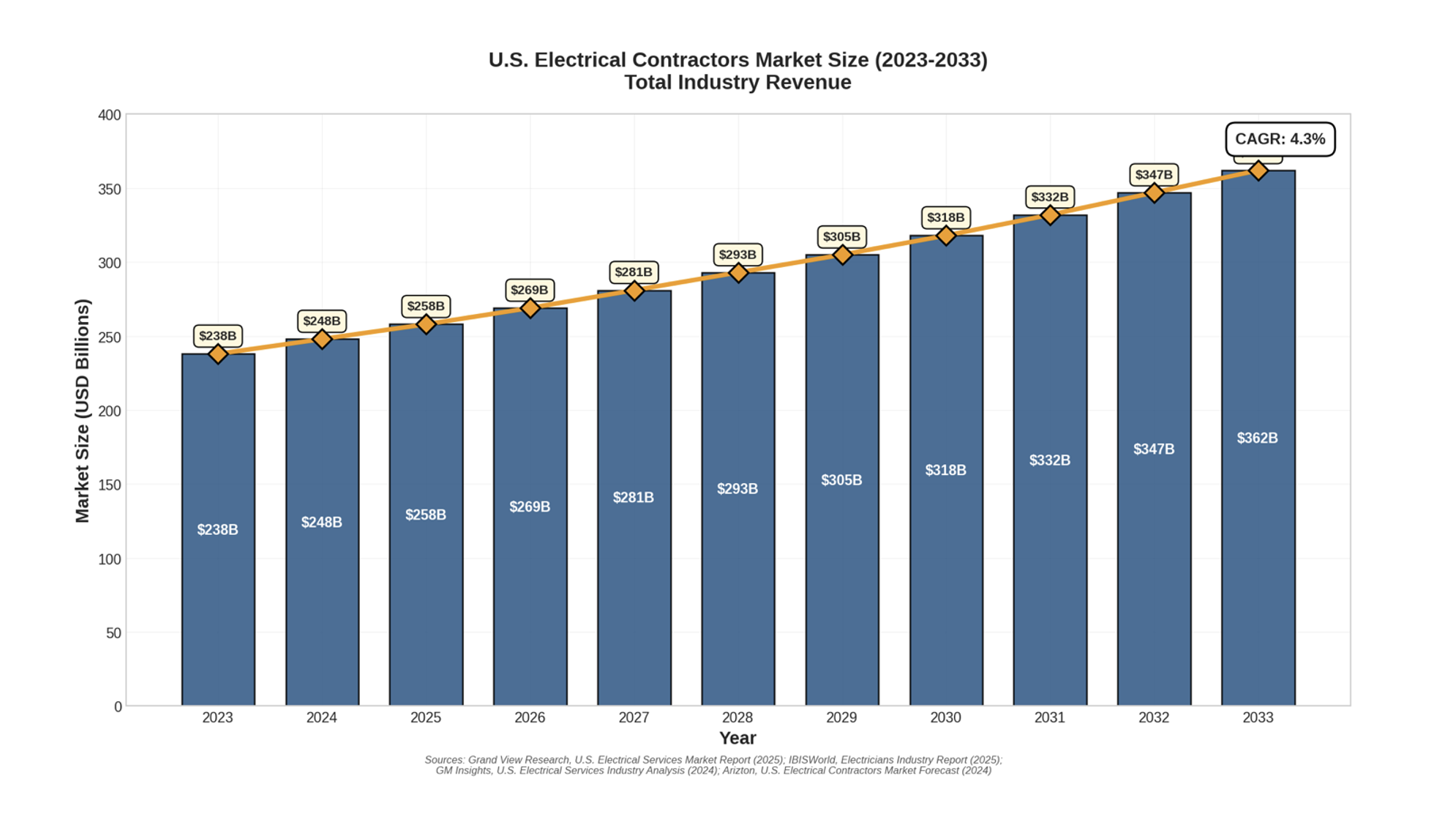

Electrical contracting is a large and foundational trade within the U.S. construction economy. The chart below illustrates the scale of the industry in terms of total establishments and aggregate industry output:

Industry revenue has historically grown at approximately 3.7% annually. Future growth is projected at a steady 2.4% per year, supported by commercial construction activity, institutional investment, infrastructure modernization, and expanding electrification demand. Although elevated interest rates have slowed residential construction, commercial and public-sector electrical work has remained resilient, aided by government-funded infrastructure programs and private investment in data centers and logistics facilities.

Key long-term growth drivers include:

Across nearly every forecast, electrical contracting is viewed as a stable and economically defensible trade anchored by essential infrastructure demand and rising technical complexity.

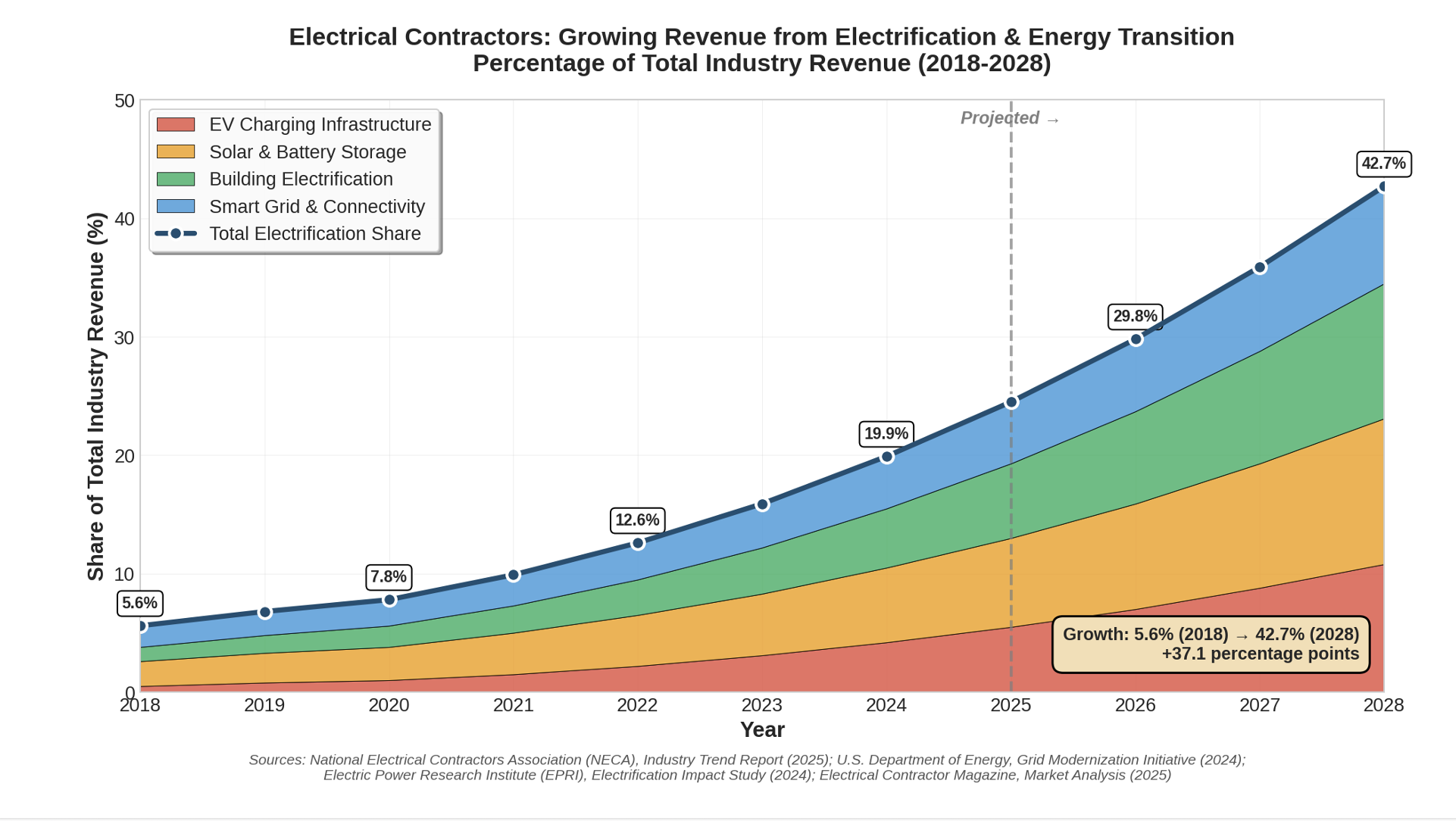

The transition toward electrified energy systems is reshaping demand for electrical contractors. Installation of EV charging infrastructure, solar and battery storage systems, building electrification upgrades, and smart-grid connectivity increasingly require specialized electrical design, compliance expertise, and licensed oversight. These projects tend to be higher-value engagements that favor contractors with advanced technical capabilities and strong safety credentials.

Electrification initiatives are reshaping demand for electrical contractors across multiple project types. The chart below highlights the growing share of industry revenue attributable to energy-transition-related projects:

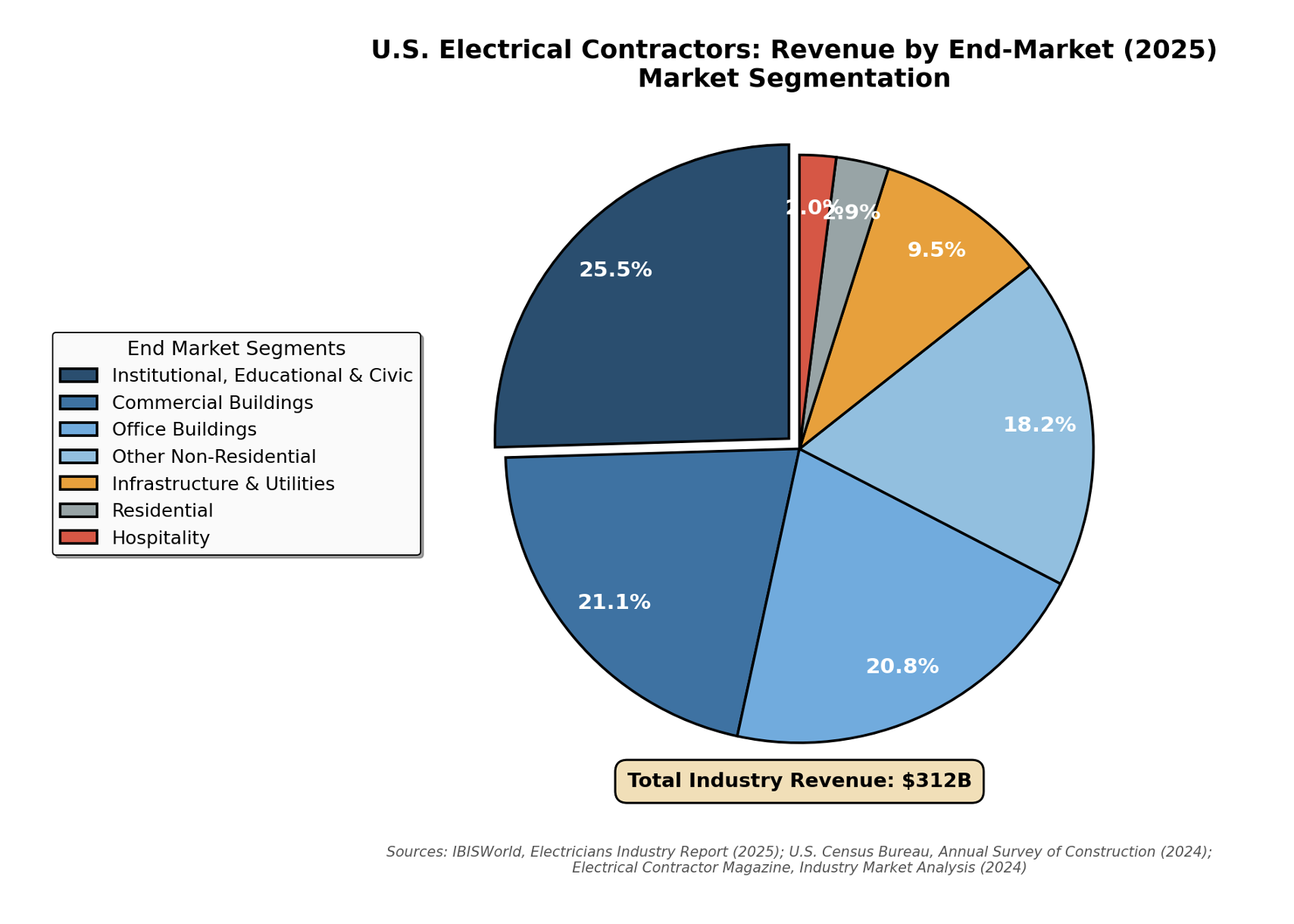

Electrical contractors also benefit directly from sustained investment in public infrastructure, healthcare facilities, educational campuses, transit systems, and municipal utilities. These end markets provide stable multi-year project pipelines and reduce exposure to short-term economic cycles.

Electrical contractors serve a diversified set of end markets. The chart below shows revenue distribution by major end-market category:

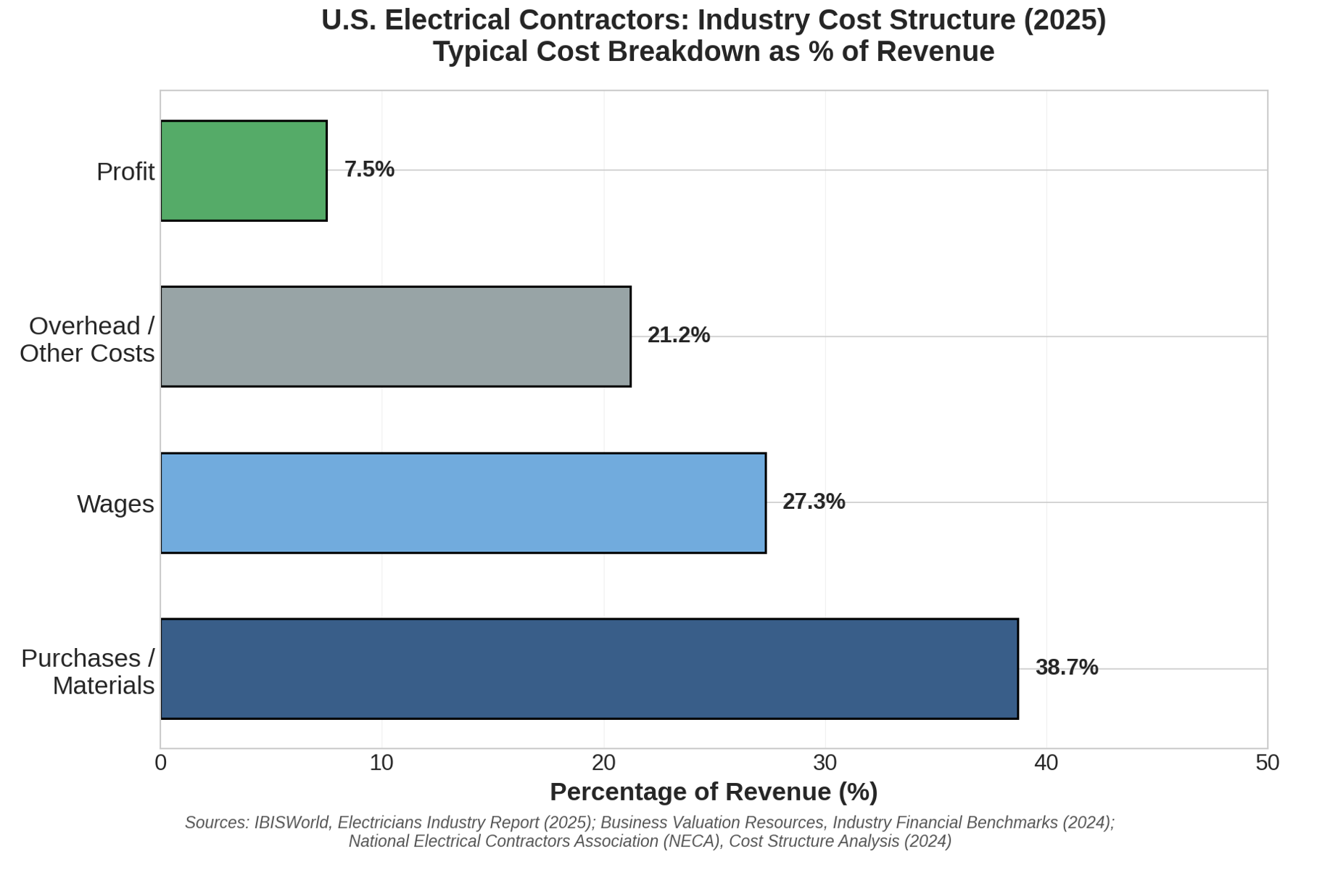

Margins in electrical contracting are driven primarily by labor availability, material costs, project execution efficiency, and bidding discipline. Skilled labor shortages remain the largest operational constraint, while material price volatility can impact profitability when escalation clauses are not embedded in project contracts.

IBISWorld benchmark data indicates:

Profitability in electrical contracting is heavily influenced by labor and material inputs. The chart below illustrates the typical cost structure across the industry:

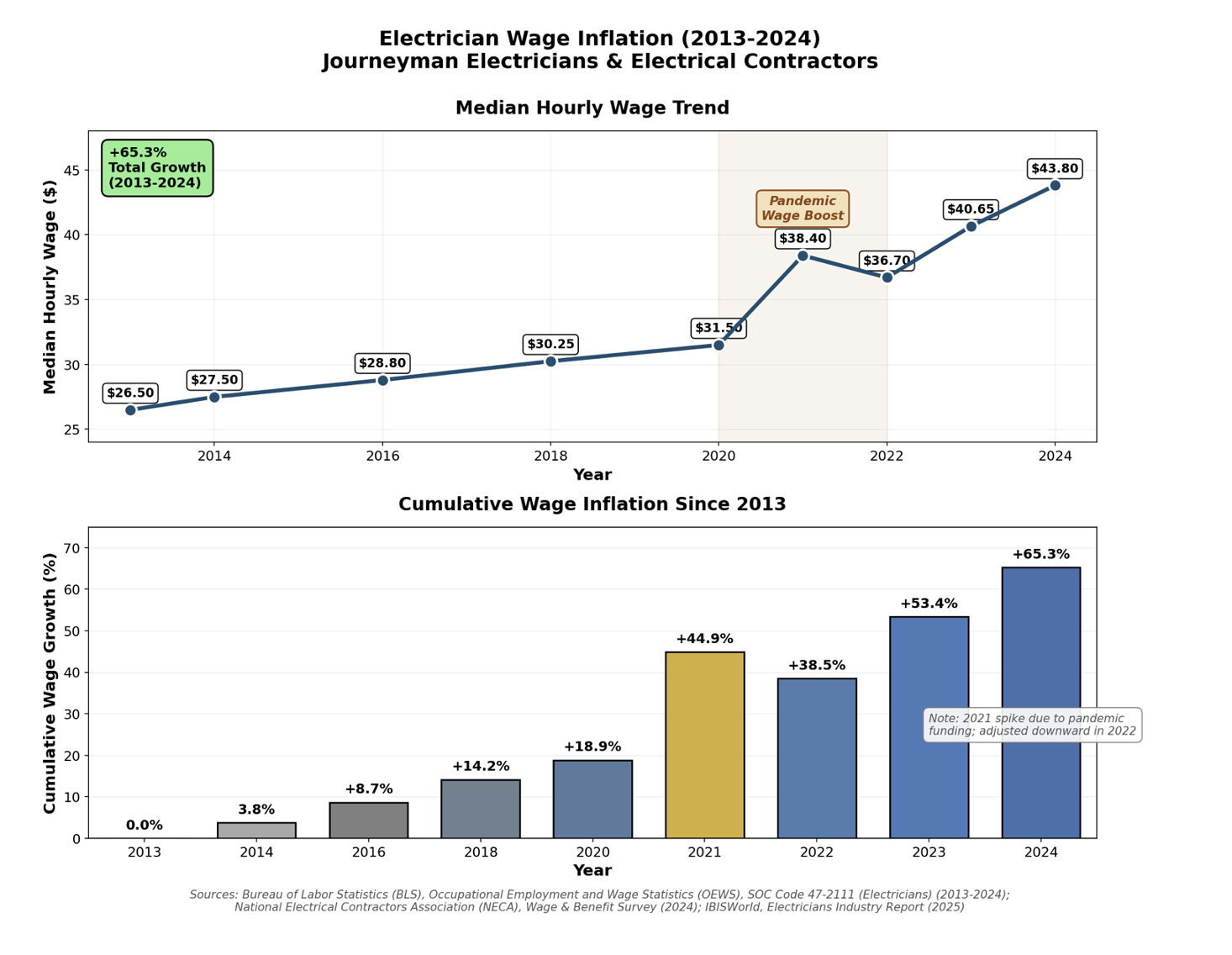

Skilled labor remains the most significant cost driver in electrical contracting. The industry continues to face a persistent shortage of licensed electricians, driven by an aging workforce, limited trade-school enrollment, and strong demand from infrastructure, energy-transition, and commercial construction projects. As a result, wage inflation has materially increased operating costs for contractors over the past decade.

Rising labor costs have compressed margins for firms lacking disciplined estimating practices or escalation clauses in project contracts. Conversely, contractors that maintain stable workforce pipelines, competitive compensation structures, and efficient project management have been better positioned to protect profitability.

The charts below illustrate median electrician wage growth and cumulative wage inflation over the past decade:

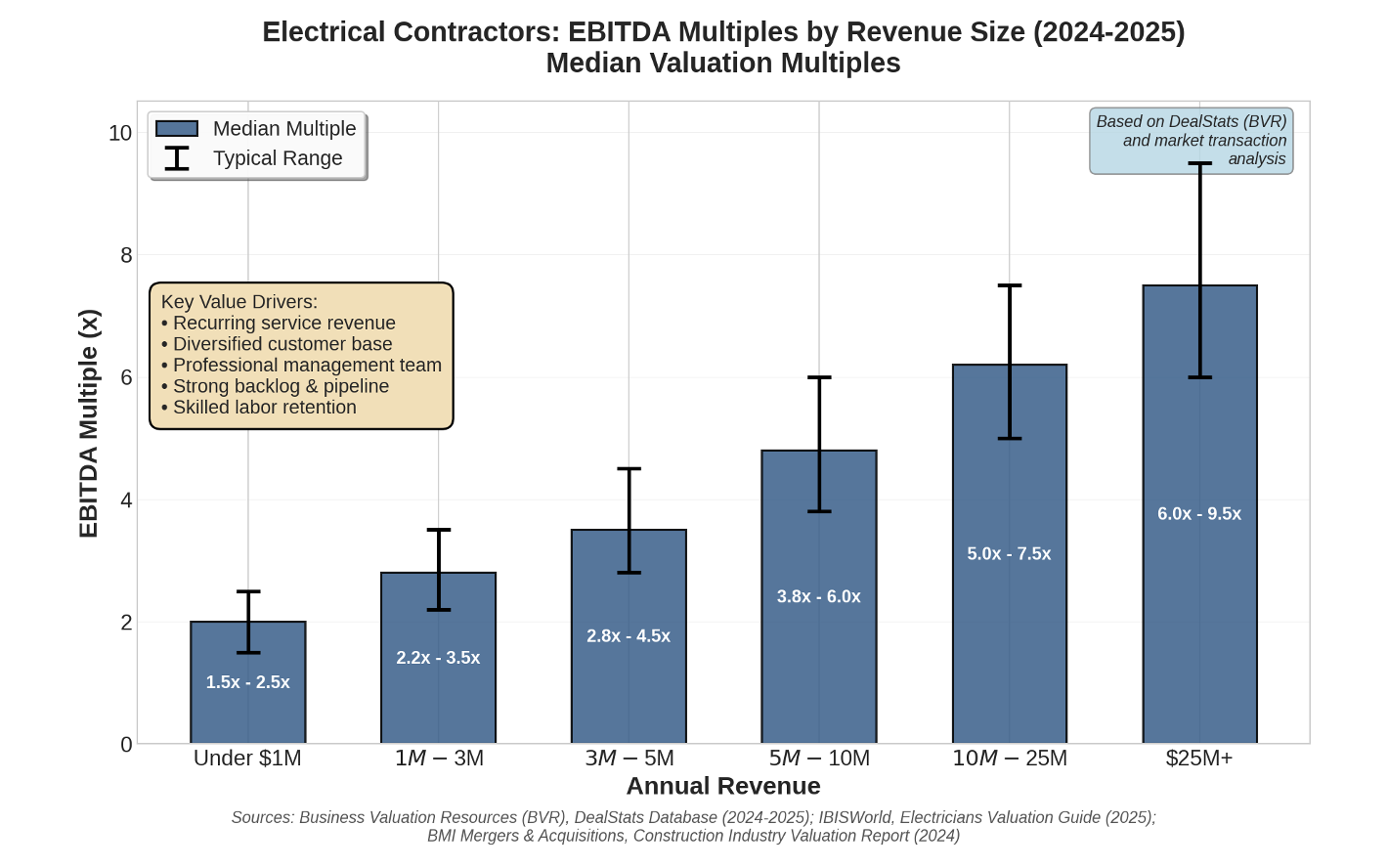

Valuation multiples in the electrical contracting industry vary significantly based on company size, backlog visibility, licensing footprint, end-market diversification, and depth of management infrastructure. Contractors with stable project pipelines, disciplined estimating practices, and strong skilled-labor retention consistently command premium valuations, while smaller owner-operated firms trade at lower multiples due to customer concentration and reliance on key individuals.

Current buyer demand remains robust, driven by private equity-backed construction services platforms, large regional contractors, and infrastructure-focused strategic acquirers seeking geographic expansion and workforce scale.

Market valuation benchmarks indicate:

The electrical contracting industry is being reshaped by the transition toward electrified energy systems. Growing demand for EV charging infrastructure, solar and battery storage installations, building electrification retrofits, and smart-grid connectivity is driving higher-value project opportunities for contractors with specialized technical capabilities.

Sustained public investment in utilities, transit systems, healthcare facilities, and educational campuses is creating stable multi-year project pipelines. These end-markets reduce exposure to short-term commercial construction cycles and provide predictable revenue backlogs.

Private equity groups and strategic acquirers are increasingly targeting well-run regional electrical contractors to build scaled platforms. Contractors with strong management teams, repeat customer relationships, and diversified project portfolios continue to attract premium buyer interest.

Leading contractors are adopting digital estimating tools, project management software, and prefabrication workflows to improve efficiency, manage labor constraints, and enhance margin predictability.

The majority of lower-middle-market electrical contracting transactions below approximately $10 million in enterprise value are financed using SBA-backed acquisition loans. Typical deal structures include:

In most transactions, sellers retain working capital such as accounts receivable and cash, while buyers acquire the operating entity and fixed assets. SBA loans generally carry 10-year amortization terms, with interest rates structured as Prime plus 1.5–2.5%. Lenders favor buyers with experience managing labor-based service businesses, familiarity with project-based cash flows, and knowledge of licensing and regulatory requirements.

Seller financing remains common, though in competitive sale processes its role is increasingly limited. Buyers still view seller notes as a signal of seller confidence and a tool to align post-close transition incentives.

Transactions exceeding approximately $10 million in enterprise value typically shift away from SBA financing and toward institutional capital structures. Buyers in this segment include private equity funds, family offices, and strategic acquirers building scaled contracting platforms.

Financing structures commonly include:

These transactions favor contractors with professionalized management teams, diversified customer bases, multi-location operations, and strong project execution systems. While valuations are often higher at this level, access to institutional buyers requires scale, reduced owner dependence, and consistent cash-flow visibility.

The electrical contracting industry is positioned for sustained growth over the coming decade, supported by electrification initiatives, infrastructure modernization, and energy-transition investment. Demand for EV charging networks, renewable energy installations, grid upgrades, and building electrification retrofits is expected to remain strong and provide long-term project pipelines.

At the same time, persistent labor shortages and wage inflation will continue to pressure margins, favoring contractors with strong workforce development programs, efficient project execution systems, and disciplined estimating practices.

Ongoing industry consolidation is expected as private equity and strategic buyers pursue scalable platform investments. Contractors with diversified end-markets, professionalized management teams, and exposure to higher-growth electrification projects are likely to attract continued buyer interest and premium valuations.

Overall, sector fundamentals remain favorable, with long-term demand drivers supporting continued M&A activity and investment in well-positioned electrical contracting businesses.

The electrical contracting industry is positioned for continued long-term expansion, driven by electrification initiatives, infrastructure modernization, and sustained investment in energy-transition projects. While labor shortages and wage inflation present ongoing challenges, these dynamics also reinforce demand for well-run contractors capable of delivering complex, compliance-intensive projects.

Professionally managed contractors with demonstrable earnings quality, diversified end-markets, strong safety and compliance records, and disciplined project execution are achieving premium valuations in today's market. For many owners, the current environment represents an attractive window to maximize value — before further labor cost escalation and competitive pressures compress margins for smaller, owner-dependent operators.

Northeastern Advisors is an independent M&A advisory firm serving lower-middle-market business owners and acquirers. We specialize in advising founder-led and privately held companies on business sales, capital raises, acquisitions, and strategic alternatives, with a focus on disciplined analysis, confidentiality, and senior-level execution throughout the transaction process.

Within the electrical contracting sector, we work with owners seeking to monetize their businesses, raise growth capital, or pursue acquisitions to scale operations. Our team has deep experience positioning service-based contracting companies for sale, preparing valuation analyses, running competitive buyer processes, and structuring transactions that maximize value while ensuring smooth post-close transitions.

We maintain an extensive network of strategic acquirers, private equity firms, family offices, and operator-backed investment groups actively seeking to invest in and acquire electrical contracting businesses. This connectivity allows us to efficiently match high-quality operators with well-capitalized buyers and deliver premium transaction outcomes.

For confidential discussions regarding valuation, market conditions, or strategic options, interested parties may contact the firm directly.

Northeastern Advisors

www.northeasternadvisors.com

us@northeasternadvisors.com

(212) 931-6070